Enter Structured Notes.

You may not have heard of structured notes. Until now, they’ve only been available to ultra high net worth and institutional investors. We’ve changed that. True to our mission, we have created a product that provides the Yieldstreet community with the potential benefits of allocating to structured notes within a portfolio, at a fraction of the historical cost.

What to consider when investing in Structured Notes?

Structured notes can be income and/or growth focused and their performance is tied to the performance of an underlying asset, and for the purpose of this article let’s use an income focused structured note tied to the performance of Mastercard stock as our hypothetical case study. This article will make it clear that coupon payments received over the life of the investment and principal repayment at maturity are dependent on the price of Mastercard stock remaining within a specified price range on each observation date.

As such, consideration must be placed on the selection of the underlying stock. Choose a highly volatile stock and you might be offered a high coupon rate but the chance of the downside protection value being breached is also higher. And we know that if the downside protection value is breached on an observation date then coupon payments will be missed.

To help mitigate the risks involved with holding structured notes within your portfolio, a diligent selection criteria should be applied when selecting the underlying asset. The goal of this process is to help ensure that the underlying stocks have fundamental and technical characteristics at the time of selection that are expected to minimize the likelihood of any significant price decline.

So what are income structured notes?

Often issued by major banks like Goldman Sachs and Morgan Stanley, income structured notes (income notes) are hybrid securities that are issued as debt, but whose outcomes are tied to the performance of an underlying asset, for example a single stock. Each individual income note pays a set coupon on a predetermined schedule, while providing a level of downside protection.

Irrespective of the underlying asset that an income note is tied to, every note has four main components that should be considered prior to making an investment. As an example, here’s how the four main components of an income note tied to the performance of Mastercard stock work in practice.

The underlying asset that the income note’s performance is tied to is a single stock, in this case, Mastercard stock. The performance of the income note is determined by the value of Mastercard stock at each observation date relative to the strike price of the structured note, i.e., the price of Mastercard stock the day the structured note was purchased.

While income note maturities can vary, for this hypothetical example let’s assume this income note matures in 18 months time.

The downside protection value of income notes can also vary. For this example, let’s assume that the downside protection value is 25%. That is, the value of the underlying Mastercard stock can fall 25% from its value on the day that the income note was purchased before coupon payments and full principal return are impacted.

Income notes pay income in the form of coupons. Coupon payment frequency and amount can vary, so for this example let’s assume that the Mastercard income note pays coupons on a quarterly basis at an annualized rate of 12% (3% per quarter).

Given that this structured note pays quarterly, it will also have quarterly observation dates. At each observation date, the then-current price of the underlying Mastercard stock will be compared to the price of Mastercard stock at the date that the income note was purchased.

How does the stock price of Mastercard influence the structured notes performance?

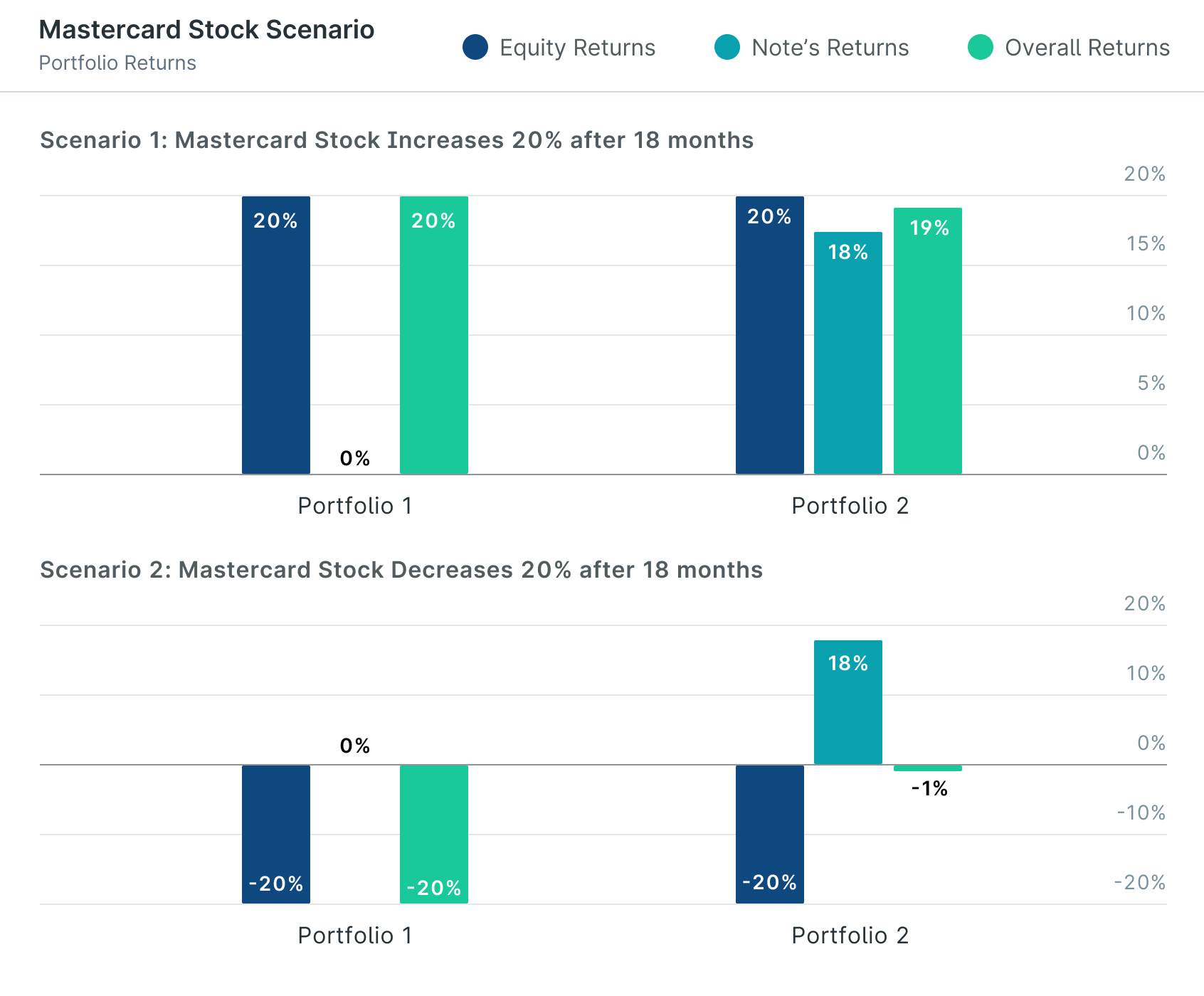

Scenario 1: Mastercard stock trades above the downside protection value of the income note for the full term

If at each observation date (including the final observation date, which is the date that maturity of the income note is set to occur), the price of Mastercard stock is trading no more than 25% less than the price of the stock on the day the income note was purchased, then coupons will be paid in full and so will full principal.

Scenario 2: The Mastercard stock price falls below the downside protection value on one/multiple observation dates but recovers

In this scenario, if the price of Mastercard trades below the downside protection value at any of the observation dates (excluding the final observation date/maturity) throughout the income note’s life, the coupon will not be paid for that period. If the price of Mastercard recovers and then begins to trade above the downside protection value by the next observation date, the full coupon will be paid and if the price remains above the downside protection value at maturity then full principal will be repaid.

Scenario 3: The Mastercard stock price falls below the downside protection value on one/multiple observation dates including the final observation date.

In this scenario, coupons will not be paid every time that the downside protection value is breached on an observation date. If the price recovers in time for the next observation date then the coupon will be paid, but if at maturity, the downside protection value has been breached again, then principal loss will occur. If the downside protection value is 25% and the price of Mastercard stock is trading 30% below the price of the stock on the day that the income note was purchased, then investors will only receive 70% of their principal investment back.

How income notes provide risk mitigation

There are three potential outcomes to an investment in income notes. While principal loss is a risk, the built-in protection helps optimize the risk/return profile for an investor. Imagine if you held Mastercard stock and it fell up to 24% over an 18 month period. Your holding would subsequently fall by this amount. However, if you held an income note tied to the performance of Mastercard in this situation, then you would still receive your 12% annualized yield and your full principal at maturity because the price remained above the downside protection value for the entire term. If you hold the two investments (single stock and income note) in conjunction with each other, then the price of Mastercard stock falling would not be so dire.

What to consider if a note has matured below barrier?

As mentioned above, if a note is below its barrier at its final observation date, investors’ principal will be affected by an amount equal to the percentage below the price of the stock on the day the income note was purchased (strike price). For example, if the downside protection value is 25% and the price of your note trades 30% below the strike price on the final observation date, then you will only receive 70% of your principal investment back for this note.

At the final observation date, should a note be trading below its barrier, investors may consider:

- Investing in the stock outright- If a stock’s price is below the note’s barrier value at the time of its final observation date and you believe the stock is worth more than it is currently trading for, you may consider investing in the stock and participate in the potential recovery. Having a realized loss on the note may help offset future capital gains taxes on a direct purchase of the stock or on other investment gains.

- Diversifying your structured notes portfolio – Diversification is one of the most commonly-used methods for reducing risk in your portfolio. The same methodology for diversifying stock holdings can also be applied to income structured notes – across themes, maturities and names. Yieldstreet aims to have one income structured notes portfolio open for investment at all times – check out our marketplace for open offerings.

What's Yieldstreet?

Yieldstreet provides access to alternative investments previously reserved only for institutions and the ultra-wealthy. Our mission is to help millions of people generate $3 billion of income outside the traditional public markets by 2025. We are committed to making financial products more inclusive by creating a modern investment portfolio.

2 Represents an net annualized return, using an internal rate of return (IRR) methodology, with respect to the matured investments shown in your Portfolio experience, utilizing the effective dates and amounts of subscriptions and distributions to and from the investments, net of management fees and all other expenses charged to the investments.[read more]