“Be fearful when the market is greedy, or be greedy when the market is fearful” – The famous maxim, attributed to Warren Buffett plays on an important idea: take advantage of extremes in investor sentiment. The market can swing wildly, and when the perception of risk deviates too far from the actual risk, there will likely be attractive investing opportunities.

Distressed investing is a classic example of this principle in action. In essence, distressed investing is an investment strategy in which investors, typically hedge funds or private equity managers, seek out companies that are in financial trouble or on the verge of bankruptcy, and seek to aid these companies in a successful turnaround. While this may seem foolhardy, when executed correctly the strategy can lead to potentially meaningful returns. This is due to the perception of high risk generally associated with companies in financial duress.

However, not all companies facing financial uncertainty are necessarily doomed. Throughout the years, there have been countless examples of companies that have either faced financial hardships or have even gone through bankruptcy proceedings and have emerged successfully. An important question to ask is whether the underlying company’s business is viable – and potentially profitable – if it were able to alleviate its challenged financial position.

Successful managers in the space have historically been able to identify these opportunities and lend their expertise and experience to help distressed companies successfully navigate the path to financial repair, oftentimes achieving attractive returns in the process.

Distressed investing offers a chance to do well in most markets as potential returns are tied to company-specific events and not necessarily the broader market. However, the number of distressed opportunities rises with the economic tide as macro or industry-specific headwinds tend to expose companies during downturns. This means the more difficult the market environment, the more likely opportunities will emerge.

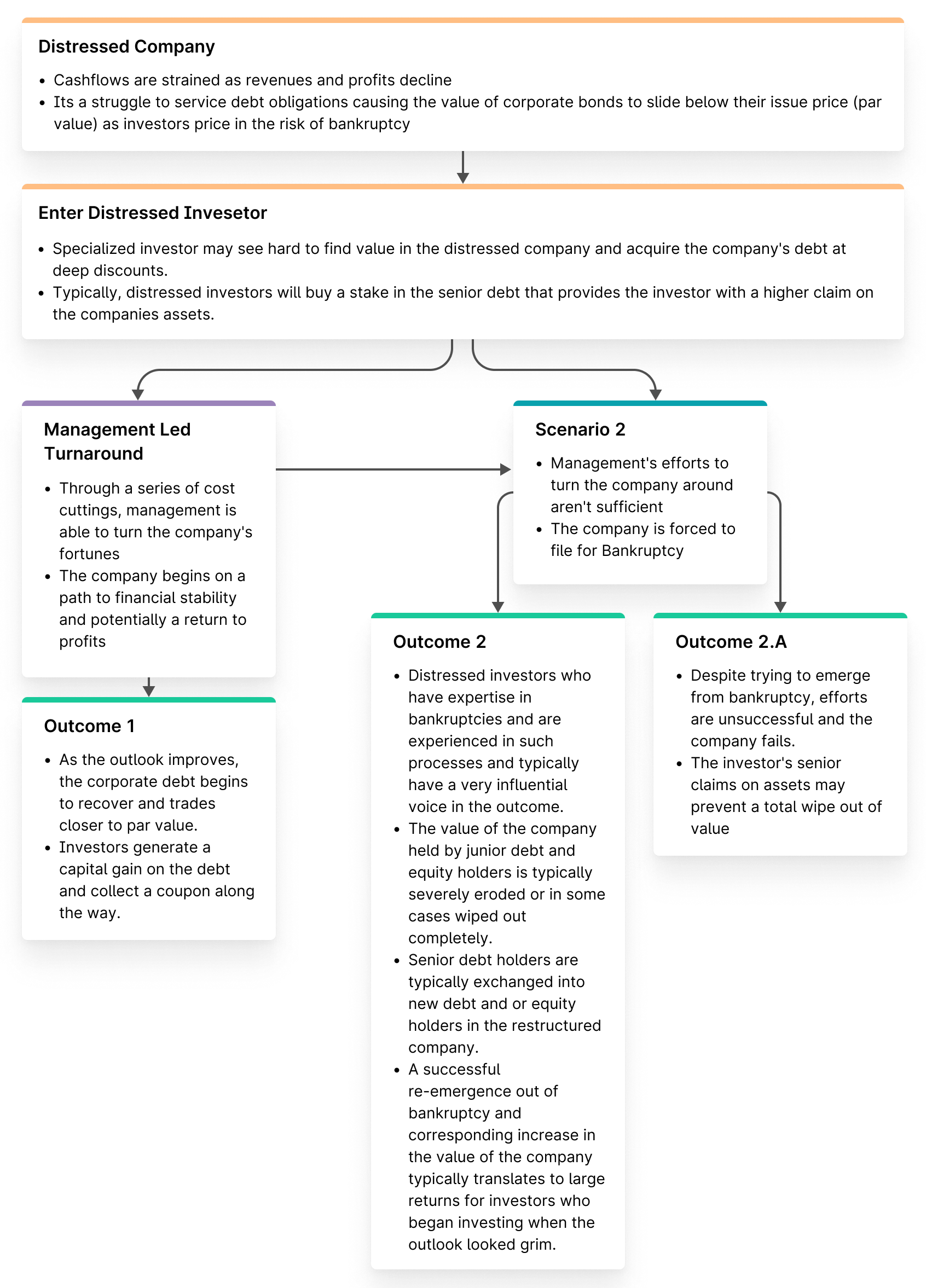

An illustrative view of distressed investing

In this hypothetical, let’s assume a company, we’ll call it Company X, has historically been a fairly well managed company. In an effort to continue growing, Company X went on an active buying spree, acquiring other companies to help improve its market share. Since interest rates were low, the acquisitions were financed via new debt and correspondingly increased the Company X leverage. For a period of time thereafter, Company X continued to maintain moderate growth and was cash flow positive, including debt servicing expenses.

In normal times Company X may have continued to operate business-as-usual, but instead, there is a significant macroeconomic event and demand for the company’s products plummets. Cash flows turn negative and the company is struggling to meet its debt servicing expenses, and its leverage ratios continue to increase as revenue and profits decline. As such, the senior corporate bonds issued by the company have traded down materially from their issue price (par) as the market is now pricing in the likelihood for bankruptcy. We’re now officially in a distressed event.

At this point, the distressed investor, we’ll call them Investor X will likely become interested and begin to evaluate the company. Investor X will model potential outcomes, including upside and downside scenarios and if the expected risk/return is favorable, then Investor X will likely build a position in the company’s debt. Most often, the distressed inventors will buy a meaningful position in a company’s most senior debt since this ranks higher in the company’s capital structure and will therefore have a higher claim on the company’s underlying assets. In this example, let’s say that Investor X did take a meaningful position in the company’s senior bonds.

As time passes, Company X is likely to try one of two paths, the first is a management led turnaround where the company pulls available levers in an attempt to avoid bankruptcy and escape their financial troubles. In this scenario, if successful, the bonds would likely recover a portion of their price over time as the market begins to have higher conviction in Company X meeting their debt obligations. If unsuccessful, the company will likely need to enter into bankruptcy proceedings.

In the second scenario, Company X enters into bankruptcy proceedings. In such an event, the company’s creditors, who have claims on the company’s assets, will begin to have a material influence. Often, a steering committee is established to help find a workable solution to allow the company to emerge from bankruptcy. Distressed investors, such as Investor X, who have expertise in bankruptcies and are experienced in such processes, typically have a very influential voice in the outcome. In a successful exit for the distressed investors, junior debt and equity are likely to be severely eroded or wiped out altogether, leaving the company with less debt.

For Investor X, this is typically how returns can become quite substantial as their initial investment in the distressed bonds of a company on the brink of failure have been turned into some combination of debt and/or equity in a newly emerged company in a less precarious financial position.

There is a third scenario as well, one in which no good outcome is achieved and the company does not emerge from bankruptcy and is forced to liquidate. In this scenario, losses may be incurred by all stakeholders, but often the most senior debt holders may achieve some form of recovery as assets are liquidated and sold off for cash, enabling for a partial repayment.

The illustrative case study above is not representative of all distressed investing outcomes. Many times, companies in such distress are there for a reason and despite the benefit from a potential restructuring, the company never recovers and continues to fail.

What's Yieldstreet?

Yieldstreet provides access to alternative investments previously reserved only for institutions and the ultra-wealthy. Our mission is to help millions of people generate $3 billion of income outside the traditional public markets by 2025. We are committed to making financial products more inclusive by creating a modern investment portfolio.

2 Represents an net annualized return, using an internal rate of return (IRR) methodology, with respect to the matured investments shown in your Portfolio experience, utilizing the effective dates and amounts of subscriptions and distributions to and from the investments, net of management fees and all other expenses charged to the investments.[read more]